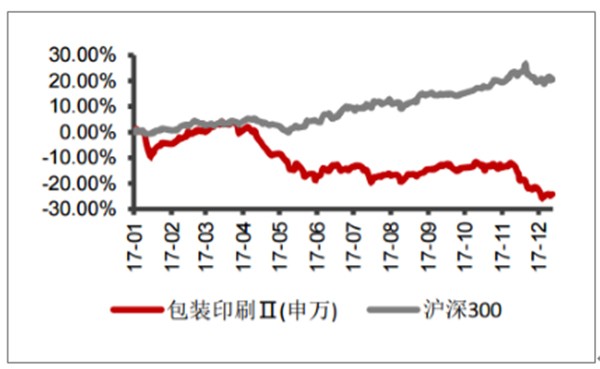

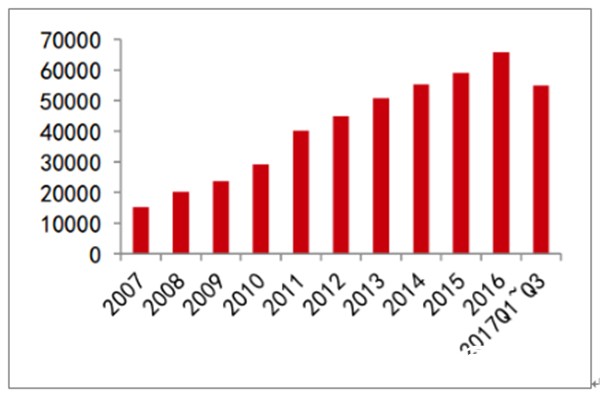

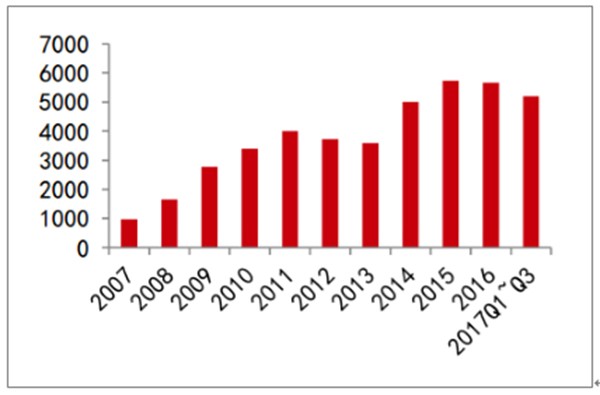

In 2017, the packaging and printing sector was sluggish. As of December 25, the overall sector index fell by 26.19%, which was higher than the average level of the light industry manufacturing sector. Overall, the performance of the packaging and printing sector was slightly stable in the first quarter and has been relatively weak since the second quarter. In the first three quarters of 2017, the revenue of the packaging and printing sector reached 54.942 billion, an increase of 15.59%, and realized a net profit of 5.193 billion, with a growth rate of 9.23%.

Packaging and printing sector fell 26.19%

Data source: public data collation

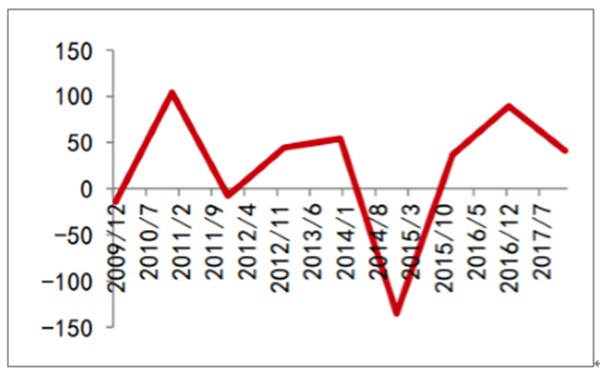

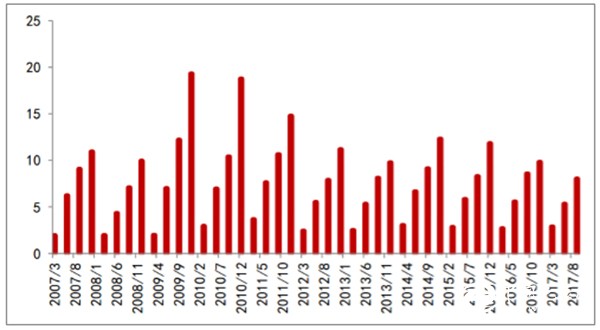

P / E ratio of packaging and printing plate

Data source: public data collation

Operating income of packaging and printing sector (million yuan)

Data source: public data collation

Net profit of packaging and printing sector (million yuan)

Data source: public data collation

In 2017, the cost of the packaging and printing sector continued to rise. Under the pressure of cost transfer, the sector as a whole was under pressure. In 2017, the return on net assets of the packaging and printing industry in Q3 was 8%, which was at a historical low in the same period of the industry.

History of packaging and printing sector ROE

Data source: public data collation

There are two reasons for the sluggish performance of the packaging and printing sector since the beginning of the year. On the one hand, the price of raw materials in the upstream has increased, especially the price of corrugated cardboard has risen sharply, resulting in a substantial increase in the cost of paper packaging. Due to the extreme fragmentation of the packaging industry, the cost of SMEs has increased and the profit space has been compressed. On the other hand, the downstream customers of packaging companies are relatively large in size and have strong bargaining power. With the overall performance of general demand this year, the overall bargaining power of packaging material suppliers is weak.

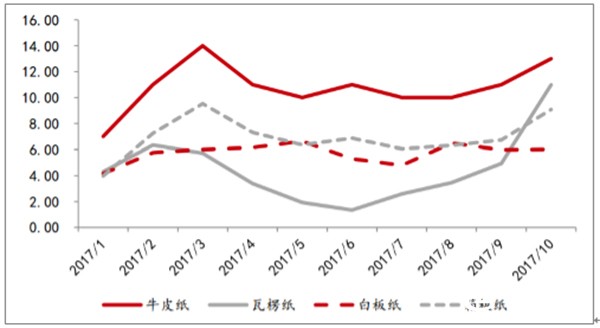

Affected by the increase in raw material prices, the gross profit margin of the packaging industry fell sharply. In the first three quarters of 2017, the price of corrugated paper increased by more than 70% year-on-year. The increase in paper prices has increased industry costs. The leading companies such as Yutong Technology and Hexing Packaging also experienced a year-on-year decline in gross profit margin. Starting from the fourth quarter of 2016, the price of waste paper began to rise. At the beginning of the year, the merchants stocked up to the middle of the year. Although the paper price rose in the third quarter, due to the demand for replenishment, the merchants prepared for the National Day Double 11 holiday, and demand expansion pulled Paper prices rose.

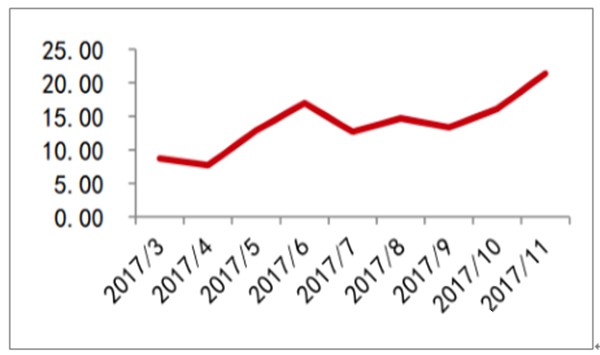

Entering 2018, we judge that the impact of the cost side on profits will be weakened. On the one hand, since the paper price rose sharply last year, the price difference between domestic and foreign papers has narrowed, and the amount of imported paper in China has started to rise. From January to October 2017, the imports of kraft paper, corrugated paper, whiteboard paper, and boxboard paper were 1.80 billion tons, respectively , 4.501 billion tons, 5.729 billion tons, and 6.948 billion tons, an increase of 27.06%, 740.58%, 6.83%, and 29.06% year-on-year, especially since the number of imports in June has continued to increase since June 2017. The increase in the number of imported paper products has effectively eased the tension of downstream demand. If paper prices continue to rise next year, the import volume is expected to remain high.

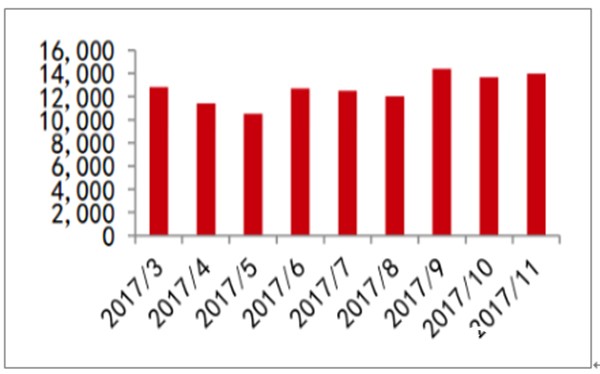

Paper imports (100 million tons) from January to October 2017

Data source: public data collation

On the other hand, the decline in industry profitability and the implementation of supervision actions have accelerated the elimination of small and medium-sized enterprises, increased market concentration, and large enterprises have gained more market share. After the promotion of the right to speak, the cost passing ability of leading enterprises will be improved to a certain extent, so the performance of paper packaging companies in 2018 is expected to usher in improvement and profitability.

The packaging and printing industry presents a typical "big industry, small company" pattern. The industry has a low barrier to entry, there are many small and medium-sized enterprises, the competition pattern is scattered, and the overall situation is oversupply, and profitability continues to decline. The threshold of the domestic packaging industry is very low, the proportion of SMEs is high, exceeding 60%, and the bargaining power of upstream and downstream suppliers is seriously insufficient.

Many packaging companies have regional characteristics, and their market shares are relatively concentrated. Even if they are the industry leaders, the market has certain limitations. In the face of poor industry prosperity, small and medium-sized packaging companies face the double pressure of rising raw material prices and limited product transportation radius, profits continue to decline, the industry supply side continues to squeeze out, backward production capacity is eliminated, and the integration of low-end paper packaging Imperative.

Taking the industry leader Hexing Packaging as an example, its main markets are distributed in Central China and South China. In 2017H1, Central China and South China accounted for 33.42% and 32.14% of the revenue respectively, but the company ’s operating income in the East China market has increased significantly in recent years. 2017H1 The proportion of operating income in East China has reached 19%.

Regional distribution of Hexing packaging business revenue

Data source: public data collation

Affected by consumption upgrades, the demand for mid- to high-end packaging is gradually strong. Packaging is an important carrier of the brand image of consumer products. The requirements for packaging of downstream consumer products will gradually increase, and high-end packaging will be used to enhance the brand image, thereby attracting more core consumer groups and grabbing high sales profits. In recent years, the demand for high-end consumer products such as consumer electronics and cosmetics is strong, and the demand for packaging paper is huge.

Supply-side reforms and consumption upgrade trends create opportunities for increasing market concentration, and packaging is also further developing toward high-end under the general trend of consumption upgrades. The demand for packaging paper for high-end commodities is becoming more and more personalized. The overall packaging integration service for high-end customers is gradually launched, and the industry business model is gradually transformed from manufacturing to service, so as to obtain higher added value.

Smartphone output (ten thousand units)

Data source: public data collation

Monthly YoY growth rate of cosmetics

Information collation: Carton Street

NINGBO BRIGHT MAX CO., LTD. , https://www.smartrider-horserugs.com